I did not discover shopper marketing in a trend report. I learned it sitting across from retailers, trying to reconcile brand ambition, trade funding, and shelf reality in the same plan. When you spend enough years in those rooms, patterns begin to emerge. The tactics change. The terminology evolves. But the underlying power shifts are remarkably consistent.

Shopper marketing did not begin with retail media networks. It did not start with digital coupons, and it certainly did not arrive with AI shopping assistants. It has been evolving for decades. The common thread through every stage is simple: whenever control of the shopper relationship shifts, shopper marketing expands and reorganizes itself around that new center of gravity.

If you follow that pattern, what is happening today feels far less like disruption and far more like continuation.

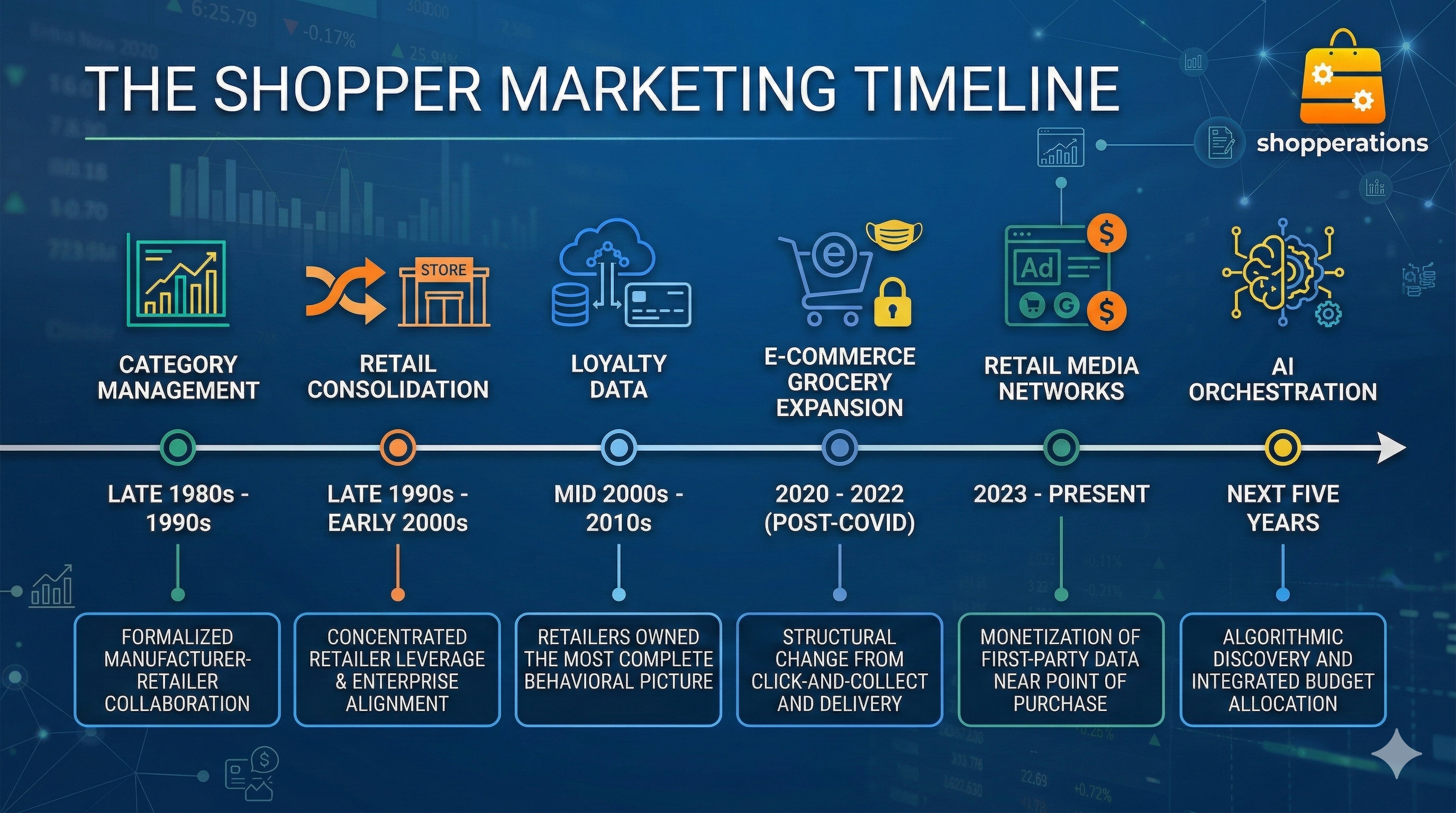

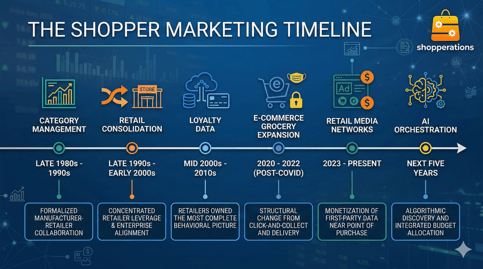

When Category Management Defined the Discipline

In the late 1980s and 1990s, Category Management formalized how retailers and manufacturers collaborated. Brian F. Harris is widely credited with pioneering the discipline and structuring the eight-step model that many of us were trained on.

CPGs were no longer simply vendors in that era. We became category advisors. We brought insights, built planograms, and recommended promotional calendars designed to grow the total category. Shopper marketing tactics such as FSIs, in-store signage, displays, and demos were integrated into those plans to drive store and aisle traffic and lift baskets.

It was often fragmented tactical work, but it lived inside a strategic framework. Brands still controlled significant national media budgets and consumer messaging. Retailers controlled the shelf. The negotiation felt balanced, even when it was tough.That balance began to shift as retail scale intensified.

Consolidation Concentrated Leverage

The late 1990s and early 2000s marked a period of aggressive consolidation. Kroger’s acquisition of Fred Meyer in 1999 is one clear example. Walmart’s Supercenter expansion reshaped grocery competition so dramatically that by 2001 it had become the largest grocery retailer in the United States.

Scale does not simply increase revenue; it concentrates influence. As retailers grew larger, fragmented planning models became inefficient. Joint Business Planning emerged less as a theoretical advancement and more as a structural necessity. P&G’s store-back philosophy reflected this shift, planning outward from retail execution rather than inward from brand calendars.

I joined Conagra during this phase and learned my craft working with Kroger. The tone of conversations was changing. What had once been category-level tactics increasingly became enterprise-level alignment discussions. Retailers expected coherence across marketing, sales, and supply chain. They craved shopper insights and rewarded those CPGs that knew how to mine and use them with a seat at the table. Shopper marketing evolved from executing category-specific promotions to running shopper-centric, thematic events that touched multiple retail departments.

Shopper marketing matured because the scale and shopper centricity demanded more coordination.

Data Redefined the Power Structure

If consolidation shifted leverage, loyalty data shifted ownership.

Kroger’s 2003 joint venture with dunnhumby is often cited as a milestone in retailer data sophistication. Transaction-level data provided retailers with granular visibility into shopper behavior, frequency, and promotional responsiveness. From that point forward, retailers increasingly owned the most complete behavioral picture.

Brands still directed large budgets, but retailers held the data that explained what actually happened at checkout. As mobile adoption expanded and digital engagement accelerated, promotional mechanisms gradually shifted toward digital formats, a trend reflected in Inmar’s reporting on promotional activity.

The infrastructure for retail media was quietly forming. Internally, however, many operating models remained siloed. Retail by retail. Brand by brand. Budget by budget. That structure functioned in a simpler environment. It strains under today’s complexity.

COVID Compressed the Timeline

E-commerce grocery had been expanding steadily, but COVID removed any remaining optionality. According to eMarketer’s forecasts, U.S. ecommerce grocery sales were expected to account for about 13.7 % of total grocery sales in 2025, up from roughly 6.2 % in 2019, meaning online share has more than doubled in just a few years as consumer behavior shifted post-COVID.

The magnitude of change was not incremental. It was structural. Retailers accelerated click-and-collect, delivery, and digital merchandising capabilities. CPG teams were suddenly expected to understand product detail page optimization, search dynamics, auction-based media buying, and near real-time performance reporting.

The velocity increased. The coordination required increased with it. And at the same time, retail media scaled aggressively.

Retail Media: Strategic Breakthrough, Operational Strain

Retail media is economically logical. When retailers own first-party data and digital real estate close to the point of purchase, monetization follows. U.S. retail media ad spending exploded over the last few years and is expected to grow to about $69.3 billion in 2026, reflecting sustained double-digit year-over-year increases.

For many large CPG organizations, retail media now represents the majority of shopper activation investment. Yet retail media also introduced significant structural complexity. Each retailer operates its own ecosystem with distinct reporting frameworks, optimization tools, and definitions of success. Agencies add additional layers. Finance requires reconciliation across platforms. Sales teams need coherent narratives for Joint Business Planning discussions.

When orchestration is weak, strategic clarity weakens with it. Instead of presenting a unified omnichannel investment story, organizations present channel summaries. Instead of elevating JBP discussions, complexity pulls them back toward tactical debates.

Retail media strengthened retailer economics. It did not automatically strengthen brand coordination.

AI Is a Layer, Not a Cure

Now the industry is leaning into AI. Walmart’s Sparky and Amazon’s Rufus AI shopping assistants are early indicators of how conversational interfaces may reshape shopper discovery. The potential is real. Retailers are applying AI to forecasting, personalization, and optimization across their ecosystems.

But AI does not correct fragmentation nor does it fix imperfect data. It depends on disciplined inputs. Optimization models require consistent taxonomy, timely data, and cross-retailer visibility. Without that foundation, AI becomes a surface enhancement rather than a structural advantage.

There is a difference between adopting technology and building operational maturity. The former is visible. The latter is decisive.

The Next Five Years

Over the next five years, retailers will likely expand monetization within AI-mediated discovery environments, integrating paid influence into conversational interfaces much as sponsored placements evolved within search. Retail media networks will continue to mature and, in some cases, consolidate, concentrating influence among the strongest platforms.

Finance scrutiny will intensify as retail media budgets grow. CFOs will expect standardized reporting, cross-retailer transparency, and defensible ROI narratives. Organizations that cannot articulate cohesive omnichannel investment strategies will feel pressure internally and in retailer negotiations.

AI-driven budget allocation will become increasingly viable, but only for organizations that have built disciplined orchestration across retailers and brands. The divide will not be between companies experimenting with AI and those that are not. It will be between companies that have invested in structural coordination and those still reconciling disconnected systems.

The Structural Imperative

Shopper marketing has matured at every inflection point in its history. From CatMan to JBP to retail media, the function expanded because the environment demanded greater coordination.

The next stage is not about chasing tools. It is about building structural alignment across retailers, brands, vendors, and media platforms. Omnichannel spend orchestration is not a reporting convenience, it is strategic infrastructure.

This is where Shopperations fits into the arc, not as a reaction to retail media or as an AI novelty, but as an operating system for modern omnichannel CPG marketing. Coordinated omnichannel spend across retailers and brands strengthens Joint Business Planning, improves financial transparency, and generates high-quality, timely data that can support meaningful optimization.

Having watched the discipline evolve from shelf-level activation to enterprise growth engine, the trajectory feels clear. Shopper marketing has moved steadily toward the center of brand and strategy. It is no longer peripheral. It is connective tissue.

The shelf is digital. The interface is becoming algorithmic. The expectations are higher. The organizations that treat shopper marketing as disciplined infrastructure will shape the next chapter. The rest will continue trying to manage complexity without organizing it.

In five years, will your shopper marketing organization look more like a media buying team, a data science team, or a strategic growth engine?